Funding

Funding is all about getting the cash for your social venture. Funding is a requirement for a venture throughout its lifecycle. For clarity it should be mentioned at the outset that here we are focusing on funds you raise from outside of the core mission of your social venture. We'll explore the function of raising finance from third parties who believe in your vision and mission, and your ability to deliver them. Access to different forms of third party funding and financing will be closely interwoven with the legal structure that you choose for your social venture– we recommend you read our guide on legal structure (if you're interested in raising investment you may also be interested in our legal structuring considerations when seeking external investment guide.

Funding from third parties may be required for several reasons, including:

- Getting you started

- Purchasing equipment

- Starting a new project

- Scaling up your activities.

Start up funding can be the hardest funding to secure. The perceived risk from the perspective of the funder is the greatest since the venture has no track record. At this stage you may have a business plan but there is no guarantee that this will translate into a sustainable business.

Sources of funding

The sources of funding are predicated by a number of factors:

- The amount of trading income you expect to generate

- The level of expected profitability

- Your venture's legal structure

If your social venture is likely to generate only or mainly social or environmental outcomes with little or no trading income then you need to consider grant funding. Strictly speaking if you are not going to generate trading income it is questionable whether you can be regarded as a social venture.

You may generate trading income but the profitability may be comparatively low compared to what a commercial business would be expected to generate. Typically social ventures also operate in markets that are high risk – e.g. environment, health, social care. Both these factors may exclude you from being funded by many commercial funding entities that are looking to invest in businesses with a higher profit potential and with a lower market risk.

You need to think through all these considerations before approaching sources of funding. You need to devise a strategy and also consider carefully what the implications of obtaining the funding sources may have on you personally and on your enterprise.

You will need to have a convincing story and outcomes to get the financial support that you need. This means that you need to have undertaken your marketing and created a business plan that explains what you intend to do, how you are going to create the social and financial returns (contained in financial forecasts) and how much you are looking for. You can get help on this from our guides on business model, marketing and financial management.

You may need to plan for staged funding – you may not be able to secure what you need immediately and from one source. This is normal. You should plan to get what you can and build on that. So you need to be looking to, and approaching, all potential sources of funding.

Set out below, are a number of funding options that one could pursue.

Personal

It is inevitable that the initial funding comes from you. The funding may be in actual cash outlay to pay for equipment, marketing, advice etc. and it will be in the time that you have put in yourself, sometimes labelled “sweat equity”.

Though the time input may be considerable it is unlikely that you have enough cash to fund your enterprise to the point that it is financially self-sufficient. (i.e. generating enough income to cover your costs).

If you are thinking of starting an enterprise it is worth saving money so that you have cash reserves for you to look after yourself and meet the requirements of the enterprise until such time as you can attract other funding or reach financial sustainability. Ensure that you keep a record of what you have spent and also the time you have devoted to the enterprise. The cash and time is your investment into the enterprise. If the enterprise structure is not share based then the cash should still be viewed as investment, but in the form of a loan, that should be repayable to you when the enterprise can afford to do this.

Friends, family, angels and fools

Often entrepreneurs turn to people that they know to support their enterprise. You may have total belief in what you want to do and what you believe you can achieve. Can you convince those around you? Is your business plan convincing enough to entice those that you know? Are you confident enough to put friendships at risk? Can they afford to part with the money? Are they only able to support you in the short term – that is, will they start demanding their money back just when you can least afford to repay them?

Having initial financial support from someone other than you makes it easier to get funding from other sources as someone else has taken the initial risk. An individual who is not part of your friends and family network, but who believes in your vision and in you enough to invest at this very early stage, is known as an angel investor. Even if friends, families and angels invest a small amount, their confidence in your enterprise may help considerably in attracting other funding.

Regardless of who your investor is, recognise that the ‘sell’ to them will be about your vision and your high level social and strategic objectives. This will be as much about selling yourself as an individual as it is about the project that you have in mind. This is a high-risk investment opportunity that you are offering, with no track record of success at this stage, and so your passion, commitment and maturity in how you discuss your plans will be crucial in convincing people that they would be backing a winner.

Finally, consider in what form this funding will take place – will it be a loan or are you willing to give shares to these initial funders? Both considerations have an impact on your enterprise. A loan is repayable and you will also need to pay interest, so it can affect your cash flow. An equity investment is only possible if you have a company with shares. The early investors may have their equity holding diluted by future investment or they may want to be bought out when someone else invests. You need to make sure you know what your investors’ motivations and repayment / exit strategies are.

Working capital/overdrafts

The most common external source of start up funding is bank finance. Usually this is in the form of an overdraft. An overdraft is a short-term form of funding for meeting an enterprise’s working capital requirements – the cash you require to pay liabilities whilst you wait to receive the money you are owed. Working capital / overdraft facilities are important for organisations that are profitable but have periods when their cash balance is close to or below zero due to the nature and timing of their payments and receipts. Many new social enterprises will fall into this category.

Banks, as is well known, are not great risk takers. The bank needs convincing that the overdraft facility given to you is not an unacceptable risk. They will want a business plan. They will want to have some form of guarantee of repayment in case the enterprise fails. You may be required to give a personal guarantee. Also beware banks can recall an overdraft at any time. They often do this at a time when you need their support the most.

The amount of overdraft facility that will be available for a start up is likely to be small and so it may only be part of the solution to your funding requirement.

There are an increasing number of social banks who understand social enterprise and are more supportive of them than the high street banks. They also bring contacts and networks that can help your enterprise. The prominent social banks are listed below:

- Unity Trust Bank – www.unity.co.uk

- The Co-Operative Bank – www.co-operativebank.co.uk

- Triodos Bank – www.triodos.co.uk

Loans

Loan finance is an option when you want a larger sum of money to start your enterprise. Loan finance is appropriate only where there is a good possibility that the loan can be paid back. You will need to repay the loan plus interest. So you must be sure you can manage this as well as convince the lender of this. Once again your business plan and financial forecast are going to be of great interest to the lender.

The advantage of loan finance is that it is contractual agreement with the lender. The lender can only demand the money back early if you do not keep up your agreed repayment schedule. Usually business loans are repayable over a number of years. Again consideration should be given to social lenders, as they are more likely to work with you to overcome any repayment problems. In many cases they will also not require personal guarantees to secure the loan. They are more open to managing the risk of lending to social enterprises than are commercial banks.

Research the lenders and ensure that you meet their lending criteria and that they can accommodate the amount you want to borrow. Some of the lenders have changing criteria as to sectors they support so you will need to check this as well.

The following lenders have a national presence:

- Unity Trust Bank – www.unity.co.uk

- Triodos Bank – www.triodos.co.uk

- The Co-Operative Bank – www.co-operativebank.co.uk

- Big Issue Invest – www.bigissueinvest.co.uk

- The Social Investment Business – www.sibgroup.org.uk

- Various local and regional community lenders (CDFI’s)

Grants

Grant funding is an attractive option for many social ventures. There is no repayment required. However grant funding needs to be carefully navigated. Grants from grant-making trusts are often restricted to organisations that are non-profit making. So many social ventures may be excluded because of their legal structure, i.e. a company limited by shares, or if the constitution states that the company is profit making. The social benefits that the enterprise will generate need to be explicit and probably measurable. The grant funders are also more demanding about wider community involvement in the ownership and governance of an organisation as well about the adequacy of governance structures.

Grants also tend to be project-specific. That is they cover the costs of delivering a project but not an enterprise’s central administration and management costs. For a startup enterprise it is exactly the administration and management costs that you need covered so that you are in a position to start delivering projects.

How we help fund ideas

Grants are usually made available to organisations and not to individuals. We're an exception, which supports individuals involved in social enterprise activity. Our start up support backs projects at the pre-startup or early startup stage. Our Do It awards offer up to £5,000 and our Grow It awards up to £15,000. Our funding is given specifically to assist the individual to realise a project, such as a one-off event, or to launch a longer term and sustainable project. We also offer budding social entrepreneurs other support in terms of workshops, networking, seminars etc.

The starting point for seeking appropriate grant making bodies is to research the following web resources:

- www.governmentfunding.org.uk

- www.trustfunding.org.uk

- www.governmentfunding.org.uk

- www.grantsonline.org.uk

- www.J4b.co.uk

- www.fundingcentral.org.uk

- www.grantfinder.co.uk

- www.grantsnet.org.uk

Equity investment

Your enterprise can only accept equity investment if it is a company limited by shares. This means you are able to sell shares to the investor. The investor could be individuals or institutions. Many institutions have minimum amounts that they will invest and tend to invest in social enterprises that are looking to grow rather than start up. As introduced earlier, the so-called angel investor may be a more likely avenue. Angels are generally successful individuals who are looking to support social enterprises and are more likely to invest in startups and invest smaller amounts.

Though equity investors will look to get a financial return for the money they have invested (i.e. a share of future profits), investors in social enterprises will also recognise that they are investing in the enterprise for it to generate a social return (and perhaps an environmental return too, depending on the business). Ensure that you understand the motivation of each of your equity investors (they will be different), including their exit strategy (i.e. how do they expect to realise the financial returns of the investment made in your enterprise?).

The social banks can either invest themselves or will be able to guide you to other sources of investment finance. More specialist investors are listed below; ensure that you have researched them before approaching them:

- Social Investment Business – www.sibgroup.org.uk

- Venturesome – www.cafonline.org

- The Big Issue Invest – www.bigissueinvest.co.uk

- Triodos – www.triodos.co.uk

- Nesta – www.nesta.org.uk/investments

- Bridges Community Ventures – www.bridgesventures.com

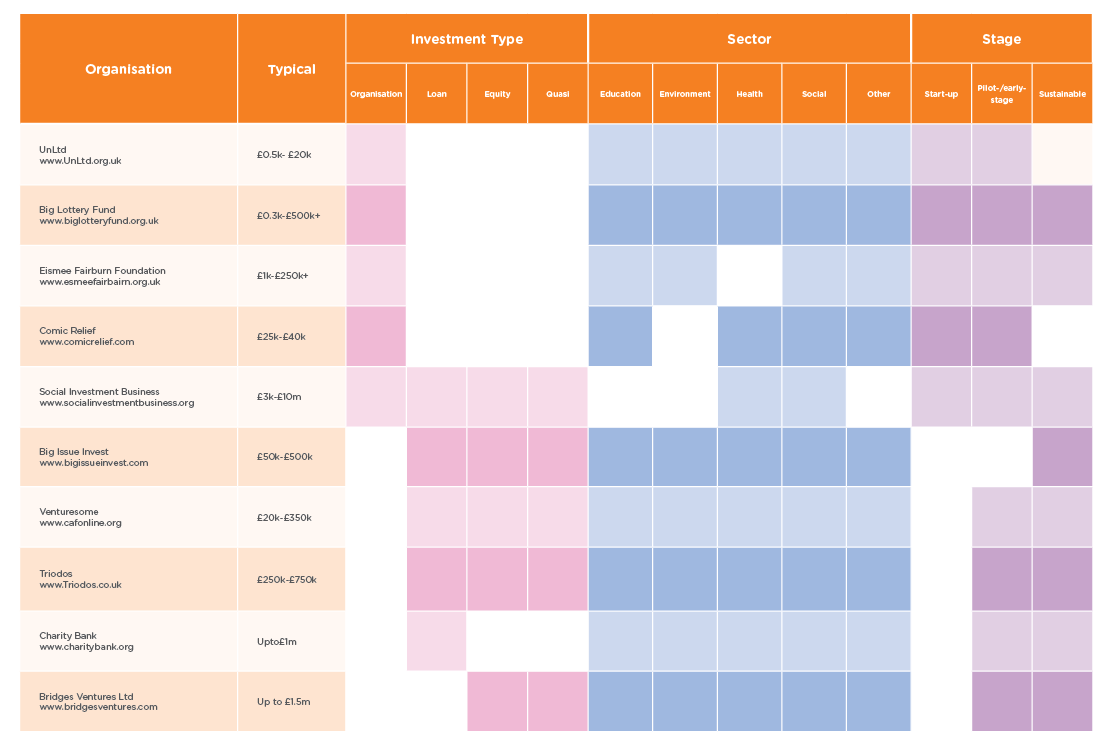

The investment landscape – an overview

The following diagram provides an overview of some of the key players in the social enterprise investment landscape. Once you have established your funding requirement and start to require more detail, try visiting the websites of these organisations directly or using one of the web-based funding search facilities mentioned above.